AVOID CAPITAL GAINS WITH OPPORTUNITY ZONES

- 10% Basis Increase If Held 5 Years

- 15% Basis Increase If Held 7 Years

- 100% Basis Increase If Held 10 Years

- Not limited to Real Estate Capital Gains

If we offered to help you with…

- Paying the minimum tax you legally owe and not a penny more (our clients pay on average 6.97% each year)…

- Increase your financial wealth and holdings (we use over 1500 tax and wealth-building strategies, all of which are 100% legal)…

- Create more cash flow in your business and personal life (so you can invest more, spend more, travel more and enjoy life more)…

- Plan for upcoming big life events and their tax impacts…

Would you take us up on that offer?

Determine If You Qualify

for Tax Deferral/Forgiveness Through Opportunity Zones

Transform Tax Savings into Wealth-Building Opportunities with QOFs

Unlimited Contribution Potential

Ever wish you could have more tax-free funds working for you in your Roth IRA? Tax-free compound growth is a great way to build wealth and is sometimes referred to as “the eighth wonder of the investing world.” The key is to maintain a long-term focus and invest as much as possible, as early as you can. Because the Roth tax savings are significant, the government tries to restrict access by imposing income and annual contribution limits. However, the soon-to-expire Tax Cuts and Jobs Act (TCJA) created a new way to enjoy tax-free compound growth without contribution caps or income restrictions: Qualified Opportunity Funds (QOFs).

How QOFs Work

QOFs offer tax-free capital appreciation until 2047 without the dollar contribution limits that slow asset accumulation in Roth accounts. Once an investor realizes a capital gain they have 180 days to invest in a QOF up to the amount of the gain. They can eliminate all capital gain liability by staying invested in the QOF for 10 years. QOFs also offer an additional deferral benefit and no penalties for early withdrawal. While these benefits may expire soon, investors who take advantage now can enjoy the potential of more than two decades of tax-free compound growth through 2047.

A capital gains liability can be deferred by reinvesting the capital gain portion of your sales proceeds in a Qualified Opportunity Fund within 180 days of realizing the gain. There is no dollar limit on how much gain can be deferred.

Although only proceeds from recent capital gains can qualify for tax deferral and possible elimination incentives,

Frequently Asked Questions

Opportunity zones - General information

What is a Qualified Opportunity Zone (QOZ)?

A QOZ is an economically distressed community where new investments, under certain conditions, may be eligible for preferential tax treatment. Localities qualify as QOZs if they were nominated for that designation by a state, the District of Columbia, or a U.S. territory and that nomination was certified by the Secretary of the U.S. Treasury via his delegation of authority to the Internal Revenue Service (IRS).

What is a qualified opportunity fund (QOF)?

A qualified opportunity fund is an investment vehicle that is organized for the purpose of investing in qualified opportunity zone properties. The IRS keeps track of investment opportunity zone tax incentive compliance through QOFs. A QOF needs to have at least 90% of its assets invested in tangible qualified opportunity zone properties to stay compliant.

What are the short-term benefits of a QOF?

The order and timing capital gains and losses are realized matters for tax planning.

- Deferment of the original capital gains taxes until the QOF is sold or through December 31, 2026. We believe there is a strong possibility that Congress may choose to extend this benefit beyond 2026.

- Control over the holding period enables our investors to implement a variety of tax-saving strategies.

What are the long-term benefits of a QOF?

Roth-like benefits without income or annual contribution restrictions.

- Elimination of all capital gains taxes, including the 3.8% NIIT, via a 100% step up in cost basis, once a 10-year hold is achieved.

- Unlike most QOFs, we don’t implement 10-year planned liquidations of the fund.

- Our investors enjoy the potential for Roth IRA-like tax-free compound growth until the incentive sunsets in 2047, which is critical to building wealth.

What is the advantage of eliminating maximum holding periods?

The biggest tax benefit offered by a QOF investment is the potential for tax-free compound growth (aka: The eighth wonder of the financial world). Once an investor achieves a 10-year hold in the QOF they can elect to step-up their cost basis 100%, eliminating any capital gain liability. This benefit is often thought of as a 10-year benefit, but that is just the beginning because the benefit does not expire until 2047 – another 23 years! Because compound growth curves accelerate in the outer years, roughly 84% of tax benefits are derived after year 10. This is a big advantage enjoyed by Park View OZ REIT investors. Unfortunately, a large majority of QOFs have planned liquidations shortly after the 10th year, ending the tax-free compound growth prematurely and forfeiting a huge potential tax benefit.

What is the advantage of eliminating investor accreditation requirements?

It makes accessing QOF tax incentives significantly easier. Because Park View OZ REIT is a public company, we have no accreditation requirements and anyone can invest in our shares. By contrast, almost all QOFs still have accreditation requirements which prohibits most of the investing public from participating. Additionally, even if you meet the accreditation requirements, turning over financial records to prove it can be a hassle and feel invasive. We believe that removing the accreditation requirement works well for our shareholders.

What are the two tax incentives offered by a QOF?

- Almost any type of capital gains liability can be deferred until the QOF is sold or December 31, 2026.

This deferral period has the potential to be extended. A bipartisan bill introduced in Congress would extend the deferral period and grandfather in existing investors. Our hope is that Congress will keep the deferral period active through a series of extensions, similar to the way they have handled New Market Tax Credit extensions.

- After holding a qualifying investment in the QOF for 10 years, any capital gain achieved by the QOF can be eliminated.

The second benefit is by far the most powerful. It allows investors to compound growth tax-free until you sell the QOF or 2047.

Who is eligible for QOF tax incentives?

Anyone who owes a capital gains liability to the U.S. government is eligible. In most cases, once the gain is realized, it must be invested into a QOF within 180 days, but there are exceptions and extensions to this rule. Importantly, unlike 1031 exchanges, you only need to invest the gain into the QOF to qualify for the tax benefit. The principal portion of your proceeds is free for any use.

What is the purpose of opportunity zone tax incentives?

The purpose of opportunity zones is to create a positive social impact by spurring economic growth and job creation in low-income communities designated as opportunity zones. It offers significant tax incentives for participating investors. States nominate communities for the designation, and the U.S. Department of the Treasury certifies that nomination. Opportunity Zones were created under the 2017 Tax Cuts and Jobs Act. There are more than 8700 designated opportunity zones located across all 50 states.

How were QOZs created?

QOZs were added to the tax code by the Tax Cuts and Jobs Act on December 22, 2017.

Have QOZs been around a long time?v

No. The first set of QOZ designations, covering parts of 18 states, were designated on April 9, 2018. QOZs have been designated to cover parts of all 50 states, the District of Columbia, and 5 U.S. territories.

What is the purpose of QOZs?

QOZs are an economic development tool—that is, they are designed to spur economic development and job creation in distressed communities.

QOZs are an economic development tool—that is, they are designed to spur economic development and job creation in distressed communities.

QOZs are designed to spur economic development by providing tax incentives for investors who invest new capital in businesses operating in one or more QOZs.

- First, an investor can defer tax on any prior eligible gain to the extent that a corresponding amount is timely invested in a Qualified Opportunity Fund (QOF). The deferral lasts until the earlier of the date on which the investment in the QOF is sold or exchanged, or December 31, 2026. If the QOF investment is held for at least 5 years, there is a 10% exclusion of the deferred gain. If held for at least 7 years, the 10% exclusion becomes 15%.

- Second, if the investor holds the investment in the QOF for at least 10 years, the investor is eligible for an adjustment in the basis of the QOF investment to its fair market value on the date that the QOF investment is sold or exchanged. As a result of this basis adjustment, the appreciation in the QOF investment is never taxed. A similar rule applies to exclude the QOF investor’s share of gain and loss from sales of QOF assets. See Q&A 26, below.

Designated Qualified Opportunity Zones

Do I need to live in a QOZ to take advantage of these tax incentives?

No. You can take advantage of these tax incentives even if you don’t live, work, or have an existing business in a QOZ. All you need to do is invest the amount of a recognized eligible gain in a QOF and elect to defer the tax on that gain.

I am interested in knowing where the QOZs are located. Is there a list of QOZs available?

. Yes. The list of each QOZ can be found in IRS Notices 2018-48 PDF and 2019-42 PDF. Further, a visual map of the census tracts designated as QOZs may be found at Opportunity Zones Resources.

What do the numbers mean on the QOZ list in Notices 2018-48 and 2019-42?

The numbers are identifiers for the population census tracts developed by the U.S. Census Bureau that are designated as QOZs.

How can I find the census tract number for a specific address? (updated October 20, 2021)

You can find 11-digit census tract numbers, also known as GEOIDs, using the U.S. Census Bureau’s Geocoder. After entering the street address, select Public_AR_Current in the Benchmark dropdown menu and Census2010_Current in the Vintage dropdown menu, and click Find. In the Census Tracts section, you’ll find the number after GEOID.

Investor questions

Qualified Opportunity Funds (QOF)

What is a QOF?

A QOF is an investment vehicle that files either a partnership or corporate federal income tax return and is organized for the purpose of investing in QOZ property.

Deferral of eligible gain

What types of gains are eligible for deferral if I invest in a QOF?

Gains that may be deferred are called “eligible gains.” They include both capital gains and qualified 1231 gains, but only gains that would be recognized for federal income tax purposes before January 1, 2027, and that are not from a transaction with a related person. For you to obtain this deferral, the amount of the eligible gain must be timely invested in a QOF in exchange for an equity interest in the QOF (qualifying investment). Once you have done this, you can claim the deferral on your federal income tax return for the taxable year in which the gain would be recognized if you do not defer it.

What are qualified 1231 gains?

In general, qualified 1231 gains are gains reported on Form 4797, Part I. For additional information, see instructions for Forms 8949 and 4797. elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.

I sold some stock for a capital gain, and during the 180-day period beginning on the date of the sale, I invested the amount of the gain in a QOF. Can I defer paying tax on that gain? (updated October 20, 2021)

Yes, this gain is an eligible gain. You may elect to defer the tax on the amount of the eligible gain invested in a QOF. If you only invest part of your eligible gain in a QOF, you can elect to defer tax on only the part of the eligible gain that was invested in this way. See Notice 2021-10 PDF for a special rule if the last day of your 180-day period was on or after April 1, 2020, and before March 31, 2021.

How do I elect to defer my eligible gain?

You may make an election to defer the gain, in whole or in part, when filing your federal income tax return. That is, you may make the election on the return on which the tax on that gain would be due if you do not defer it. For additional information, see How To Report an Election To Defer Tax on Eligible Gain Invested in a QOF in the Form 8949 instructions.

Can I defer 1231 gain for a taxable year under the QOZ rules?

Yes. You can elect to defer the amount of 1231 gain if the amount of the gain was invested in a QOF during the 180-day period that begins on the day the 1231 gain was realized. For proper reporting of this gain, see instructions for Forms 8949 and 4797. If your 1231 gain was realized in 2019, your 180-day period may begin on December 31, 2019.

Can I still elect to defer tax on that gain if I have already filed my federal income tax return?

Yes, but you will need to file an amended return. An individual or a married couple uses Form 1040-X for this purpose and attaches Form 8949.

I sold property in 2015 using the installment sale method, and I’m still receiving installment payments. If I invest the amount of the gain from payments received in 2020, can I defer paying tax on that gain?

Yes. All of your eligible gains from installment sales are eligible for deferral, to the extent they are timely invested in a QOF. The 180-day period during which to invest in a QOF begins on the day the installment payment is received, even if the installment sale giving rise to the gain took place prior to December 2017.

I sold property in 2020, and the sales proceeds will be paid to me in installments. What options do I have to make investments in QOFs to defer paying tax on that gain?

Because your installment sale took place after 2017, if you elect installment treatment for your sale, you have two options for how to defer gain.

- First, you may choose to have a single 180-day period for making one or more investments in one or more QOFs. In this case, the first day of the period is the last day of the tax year in which the sale occurred, and you make a single election to defer gain on the sale up to the amount that you invest in QOFs during that period.

- Second, you may choose to have a separate 180-day period for each installment payment. Each such period begins on the day on which the installment payment is received, and the gain with respect to each payment is deferred to the extent that an amount is invested in a QOF and you separately elect to defer that gain.

Can I elect to defer gain if I transfer property other than cash to a QOF?

Yes. You can transfer property other than cash to a QOF. However, a transfer of non-cash property may result in only part of the investment being a qualifying investment (that is, only part of the investment can benefit from the QOZ tax incentives). Specifically, the amount of gain that can be deferred is limited to the basis of the contributed property, even if a greater value of property is transferred.

May nonresident alien individuals and foreign corporations elect to defer eligible gain by making an investment in a QOF?

Yes. Nonresident alien individuals and foreign corporations may generally elect to defer eligible gains that are otherwise subject to federal income tax in their hands. For example, this includes gains that are effectively connected to a U.S. trade or business and capital gains from the disposition of a U.S. real property interest by a nonresident alien individual or a foreign corporation. If the gain would be exempt from federal income tax under an applicable income tax treaty, the foreign person must waive any treaty benefits in order to elect to defer the gain.

When I transfer property to a QOF, does my holding period for the property also transfer to my qualifying investment in the QOF?

No. Your holding period of property transferred to a QOF doesn’t transfer to your qualifying investment in the QOF for purposes of the QOZ tax incentives.

180-day investment period

When do I have to invest the amount of an eligible gain in a QOF to qualify for the QOZ tax incentives?

Generally, you have 180 days to invest an eligible gain in a QOF. The first day of the 180-day period is the date the gain would be recognized for federal income tax purposes if you did not elect to defer the recognition of the gain.

I am a partner in a partnership and the partnership sold assets generating capital gains on July 1, 2019. The partnership did not make an election to defer the eligible gain. The partnership’s taxable year is a calendar year. When does my 180-day investment period begin? Does it matter that on May 1, 2020, I received a K-1 notifying me of the gain?

The date on which you receive a K-1 notifying you of the eligible gain is not relevant. Partners in a partnership, shareholders of an S corporation, and beneficiaries of estates and non-grantor trusts have the option to start the 180-day investment period on any of the following dates:

- the last day of the partnership taxable year (December 31, 2019);

- the same date that the partnership’s 180-day period begins (July 1, 2019); or

- the due date for the partnership’s tax return, without extensions, for the taxable year in which the partnership realized the eligible gain (March 15, 2020).

On December 10, 2019, I received capital gain dividends from a Regulated Investment Company (RIC) and a Real Estate Investment Trust (REIT). I am a calendar year taxpayer. When does my 180-day investment period start for my capital gain dividend?

The date on which you receive a K-1 notifying you of the eligible gain is not relevant. Partners in a partnership, shareholders of an S corporation, and beneficiaries of estates and non-grantor trusts have the option to start the 180-day investment period on any of the following dates:

- the last day of the partnership taxable year (December 31, 2019);

- the same date that the partnership’s 180-day period begins (July 1, 2019); or

- the due date for the partnership’s tax return, without extensions, for the taxable year in which the partnership realized the eligible gain (March 15, 2020).

Basis questions

I made an investment in a QOF. After holding it for at least 10 years, I sell or exchange it. Can I adjust the basis in the QOF interest to its fair market value?

Yes, but only to the extent you made a proper deferral election with respect to your investment (that is, only to the extent that your investment in the QOF is a qualifying investment).

In connection with a proper deferral election, I made an investment in a QOF partnership. The QOF subsequently invested cash in another partnership (partnership A). Partnership A is a QOZ business, and the QOF’s investment in partnership A was solely in exchange for the interest in partnership A. After I held my investment in the QOF for 10 years, partnership A sold a building to an unrelated party for a gain. That gain is part of my distributive share with respect to the QOF and is reported to me on a K–1. May I exclude this gain?

Yes. In addition to the basis increase rules for sales of qualifying QOF interests held for at least 10 years, the holder of a qualifying investment (with respect to that investment) may elect to exclude all gains and losses generated from the sales of assets by that QOF or certain lower-tier partnerships owned by the QOF. This is permitted, however, only if all of the following requirements are satisfied:

- First, it only applies to that portion of the investment that was a qualifying investment in a QOF partnership or QOF S corporation that the taxpayer held for at least 10 years.

- Second, there was an election made to exclude all the gains and losses from the sales that are attributable to the qualifying investment on a timely filed federal income tax return. This election to exclude gains and losses may be made for each year during which there are asset sales by the QOF or certain lower-tier partnerships.

- Third, the gain from that sale was not derived from the sale of inventory in the ordinary course of a trade or business.

- Fourth, the QOF must distribute (or be treated as making a distribution of) the net proceeds from the sales within certain time periods.

I deferred an eligible gain by investing in a QOF partnership. (Thus, my partnership interest in the QOF is a qualifying investment.) The following year, this QOF partnership merged with another QOF partnership. Do I recognize any gain under the QOZ rules due to the merger?

No, provided that you only received a qualifying investment in the new partnership as a result of the merger. There may be gain recognition under the QOZ rules if you received other property as part of the merger.

I deferred an eligible gain by investing in a QOF partnership and received a qualifying investment. Another partnership in which I am a controlling partner received a profits interest in exchange for services to the same QOF partnership. How does the profits interest affect my qualifying investment?

A profits interest received in exchange for services is not a qualifying investment in a QOF. If the profits interest is held in a separate partnership, even one that is controlled by you, it will not affect your separate qualifying investment

I had ordinary gain from the sale of property in 2018. During the 180-day period beginning on the date of the sale, I invested the amount of that gain in a QOF. In 2029, I sell my interest in the QOF. Can I adjust my basis to fair market value?

No. Ordinary gain is not eligible for deferral. Therefore, your QOF investment wasn’t a qualifying investment made in connection with a proper deferral election. For this reason, the basis adjustment to fair market value isn’t available for that investment. This type of investment is called a non-qualifying investment. (It is a mixed-funds investment if the taxpayer directly holds both a non-qualifying investment and a qualifying investment in the same QOF.)

Inclusion of deferred gain questions

I deferred an eligible gain by investing in a QOF. What ends the deferral?

An investor must include the remaining deferred gain on the earlier of an inclusion event or December 31, 2026. The amount of deferred gain included in income depends on (i) the fair market value of your qualifying investment in the QOF on the date of the inclusion event and (ii) adjustments to the tax basis of that qualifying investment.

What is an inclusion event?

An inclusion event, in general, is an event that reduces or terminates your qualifying investment in a QOF.

I elected to defer eligible gain after I made a qualifying investment in a QOF, and now that QOF has liquidated before December 31, 2026. What happens to my deferred gain?

When the QOF liquidated, the deferral period ended. You must include the deferred gain in the taxable year during which your QOF liquidated. When you file your federal income tax return for that year, you must report the gain on Form 8949 and must reflect the change to your QOF investment on the Form 8997. See instructions for Forms 8949 and 8997.

I elected to defer eligible gain after I made a qualifying investment in a QOF and, before December 31, 2026, I gave the qualifying investment to my child. Is there anything that I need to do?

Yes. Giving away your qualifying investment in the QOF is an inclusion event, which ends the deferral period. When you file your federal income tax return, you must report the deferred gain related to the QOF investment. Your child has a non-qualifying investment. See instructions for Forms 8949 and 8997.

If I give my qualifying investment in a QOF to my revocable grantor trust, does that end the deferral of my eligible gain?

No. Because you are treated as the owner of the trust for federal income tax purposes (that is, because it is a grantor trust), the transfer is not an inclusion event and so does not end the deferral period. A transfer of a qualifying investment to a non-grantor trust is an inclusion event, which ends the deferral period.

In 2018, I elected to defer eligible gain after I made a qualifying investment in a QOF. In 2020, my spouse and I divorced and, pursuant to the divorce decree, I transferred the qualifying investment to my spouse. What happens to my deferred gain?

Transferring your qualifying investment to your spouse was an inclusion event, which ended the deferral period. When you file your federal income tax return for the year of the divorce, you must report the gain and the change to your qualifying investment. Your spouse has a non-qualifying investment in the QOF. See instructions for Forms 8949 and 8997.

I am a partner in a partnership that is certified as a QOF. The QOF partnership made an actual or deemed distribution of property (including cash) to me with respect to my qualifying investment on or before December 31, 2026. This distributed property has a fair market value in excess of my basis in my qualifying investment. Is this an inclusion event?

Yes. Subject to an exception for certain partnership merger transactions, the distribution that you received from your QOF partnership is an inclusion event to the extent that the distributed property has a fair market value in excess of your basis in your qualifying investment. However, this inclusion event does not prevent you from excluding from gross income any gains with respect to the remaining qualifying investment if you hold it for at least 10 years and subsequently make an election with respect to that investment. See Q&As 5 and 26.

Qualified Opportunity Funds questions

Qualified Opportunity Funds (QOF)

What is a QOF?

A QOF is an investment vehicle that files either a partnership or corporate federal income tax return, is organized for the purpose of investing in QOZ property and elects to self-certify as a Qualified Opportunity Fund.

How does a corporation or partnership become certified as a QOF?

To become a QOF, an eligible corporation or partnership elects to self-certify by annually filing Form 8996 with its federal income tax return. See Form 8996 instructions. The return with the Form 8996 must be filed timely, taking extensions into account.

Can a limited liability company (LLC) be a QOF?

Yes. An LLC that chooses to be treated either as a partnership or corporation for federal income tax purposes and is organized for the purpose of investing in QOZ property can be a QOF.

Qualified Opportunity Zone business property

When is tangible property QOZ business property?

Tangible property is QOZ business property if–

- it is used in a trade or business of the QOF or in a QOZ business;

- it was purchased after December 31, 2017;

- the original use of the property in the QOZ commenced with the QOF or QOZ business OR

- the property was substantially improved by the QOF or QOZ business; and

- during substantially all of the time the QOF or QOZ business held the property, substantially all of the use of the property was in a QOZ.

- the interest must be acquired after December 31, 2017, solely in exchange for cash;

- the corporation or partnership must be a QOZ business; and

- for 90% of the holding period of that interest, the corporation or partnership was a QOZ business.

Qualified Opportunity Zone property

What is QOZ property?

QOZ property is a QOF’s qualifying ownership interest in a corporation or partnership that operates a QOZ business in a QOZ or certain tangible property of the QOF that is used in a business in the QOZ. To be a qualifying ownership interest in a corporation or partnership,

- the interest must be acquired after December 31, 2017, solely in exchange for cash;

- the corporation or partnership must be a QOZ business; and

- for 90% of the holding period of that interest, the corporation or partnership was a QOZ business.

See Form 8996 instructions.

For a QOF, does working capital qualify as QOZ property? (added October 20, 2021)

No. For a QOF, working capital is not QOZ Stock, QOZ Partnership interest or QOZ Business Property and therefore it is not QOZ property.

The QOF recently received a large equity contribution consisting of cash. Does this cash qualify as QOZ property?

No. However, for a cash contribution received in the 6 month period before a QOF property testing date that is held in cash or cash equivalents, the QOF may choose to exclude from both the numerator and denominator of the first investment standard test calculation following the contribution.

Purchase requirement

I contributed land located in a QOZ to a QOZ business. The QOZ business plans to construct a new building on the contributed land. Can the new building satisfy the requirement that it be acquired by purchase?

Yes. The building is QOZ business property, if it meets the following requirements:

- It is intended to be used in a trade or business in a QOZ;

- The materials used to construct the new building were QOZ business property; and

- It is treated as acquired after 2017. For this purpose, the newly constructed building is acquired on the date significant physical work begins.

The contributed land on which the building is located, however, is not QOZ business property because it was not purchased by the QOF.

When does significant physical work begin?

This depends on the facts and circumstances. In this regard, significant physical work does not include preliminary activities such as planning or designing, securing financing, exploring, or researching. For example, if a factory is to be constructed on a site, preliminary activities include clearing or testing of soil condition. On the other hand, significant physical work begins, for example, when work starts on the excavation of footings or the pouring of pads for the factory

Instead of purchasing equipment to use in my QOZ business, I wish to lease equipment. Can leased property qualify as QOZ business property?

Yes. If the parties to the lease are unrelated, the leased property can qualify as QOZ business property only if—

- The lease for the property is entered into after December 31, 2017; and

- The terms of the lease are market rate (that is, the terms reflect common, arms-length market pricing in that location).

In addition, if the parties to the lease are related—

- There must be no prepayment in connection with the lease that exceeds 12 months, and

- If the leased property had been previously used in the QOZ, then, before the earlier of the last day of the lease, or 30 months after the receipt of tangible personal property under the lease, the business must freshly purchase for use with the leased property QOZ business property equal in value to the leased property.

Original use property

What is “original use” of tangible property?

Original use of tangible property occurs when the property is first placed in service in a manner that would start depreciation or amortization if the property were being used in a trade or business. The original use of tangible property is in a QOZ if the property has not previously been placed in service in the QOZ. Thus, tangible property that had been placed in service outside of the QOZ (that is, used property) can be original use property if the QOF or QOZ business is the first to place it in service in the QOZ.

I purchased a building in a QOZ that is currently vacant. Is the building “original use” property?

Vacant property (including a building) is original use property if—

- The property was vacant for an uninterrupted period of three years beginning after the date the IRS designated as a QOZ the census tract that contains the property; or

- The property began to be vacant at least one year prior to the date when the IRS designated that census tract as a QOZ, and the property remained vacant through the date of the purchase.

Substantial improvement of property

What does it mean for property to be “substantially improved”?

Property is substantially improved if, during any 30-month period beginning after the property is acquired, additions to the basis of the property exceed an amount equal to the adjusted basis at the start of the 30-month period.

A QOF purchased tangible property in a QOZ, and that property is currently undergoing substantial improvement. Is the property substantially improved as QOZ business property for purposes of the 90% investment standard?

If tangible property is undergoing improvement and its basis has not yet been doubled but the QOF reasonably believes that the property will be QOZ business property after improvements are completed, then during the 30-month substantial improvement period, the property counts as substantially improved.

My QOF, or QOZ business, purchased a hotel that is located in a QOZ. Does the parcel of land on which my hotel building is located need to be substantially improved?

If a building is used in the active conduct of a trade or business, you generally do not need to substantially improve the parcel of land on which the building is located. However, if the land is unimproved or minimally improved, the land must be substantially improved. Moreover, the land fails to be QOZ business property if it was purchased with an expectation that it would not to be improved by more than an insubstantial amount.

Substantially all” in the definition of QOZ business property

The words “substantially all” appear twice in the definition of QOZ business property. Do these words have the same meaning in both places? If not, what are the two meanings, and how do they interact?

QOZ business property is tangible property owned or leased by a QOF or QOZ business that satisfies a variety of criteria. These criteria include requirements that, during substantially all of the time in which the QOF or QOZ business holds or leases the tangible property, substantially all of the use of that property by the QOF or QOZ business must be in a QOZ. The first of these two “substantially all” references means at least 90 percent, and the second means at least 70 percent. Thus, during at least 90 percent of the time in which the QOF or QOZ business holds or leases the tangible property, at least 70 percent of the use of that property by the QOF or QOZ business must be in a QOZ. Applying these two definitions together means that, during the entire time in which the QOF or QOZ business owns or leases tangible property, at least 63% of the use of that tangible property must be in a QOZ.

I and a few employees operate a landscaping business from a building located in a QOZ. My employees and I meet at our building, receive job instructions for the day, and transport our landscaping equipment to job sites located within QOZs as well as sites that are not located within QOZs. At the end of our job, we transport the equipment back to our building and carry out the rest of our job duties. Can my landscaping equipment qualify as QOZ business property?

Yes. Mobile tangible property, such as your landscaping equipment, can qualify as QOZ business property. Because you use your landscaping equipment in multiple census tracts, you must aggregate the number of days you use the tangible property in various census tracts. Generally, if you used your landscaping equipment at least 70% of the days in QOZs, your landscaping equipment is substantially used in a QOZ. In addition, based on the way you use your landscaping equipment in your business, if you always return your landscaping equipment back to the building at least every 14 days, you qualify for a safe harbor that allows you to exclude up to 20% of your landscaping equipment from this 70% calculation. See Form 8996 instructions.

Can inventory qualify as QOZ business property?

Yes. Inventory (including raw materials) can qualify as QOZ business property. In addition, you may choose annually to exclude inventory from QOZ business property and from the denominator of the applicable determination (whether 90 percent or 70 percent). During each taxable year, whether you choose to include or exclude inventory from both QOZ business property and the denominator, you must treat all of your inventory consistently during that taxable year.

Can inventory in transit qualify as QOZ business property? (added October 20, 2021)

Yes. If inventory of a QOF or QOZ business, including raw materials, is in transit, the inventory can qualify as QOZ business property. That is, inventory does not fail to qualify solely because the inventory is in transit from a vendor to a QOF or QOZ business or from a QOF or QOZ business to a customer.

Qualified Opportunity Zone business

QOF 50-percent of gross income test

What is the 50-percent-of-gross-income test?

Each taxable year, a QOZ business must earn at least 50 percent of its gross income from business activities within a QOZ. The regulations provide three safe harbors that a business may use to meet this test. These safe harbors take into account any of the following—Q57. Must a QOZ business meet all three safe harbors to satisfy the 50-percent-of-gross income test?

- Whether at least half of the aggregate hours of services received by the business were performed in a QOZ;

- Whether at least half of the aggregate amounts that the business paid for services were for services performed in a QOZ; or

- Whether necessary tangible property and necessary business functions were located in a QOZ.

Must a QOZ business meet all three safe harbors to satisfy the 50-percent-of-gross income test?

No. A QOZ business satisfies the 50-percent-of-gross income test if it satisfies any one of these safe harbors. For example, if 50 percent or more of all the hours of services that a business receives and uses were performed in one or more QOZs, then the business satisfies the hours of services received test and, therefore, satisfies the 50-percent-of-gross-income test.

More information

How can I get more information about QOZs?

Find information and resources about Opportunity Zones, investing in a Qualified Opportunity Fund, and certifying and maintaining a Qualified Opportunity Fund.

Opportunity Zones by Location

List of Opportunity Zones by State

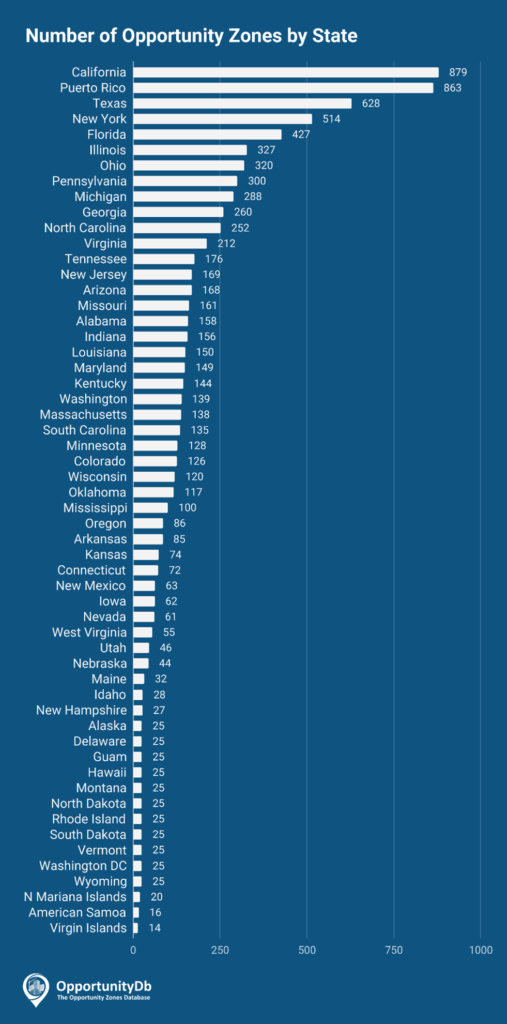

There are 8,764 opportunity zones in the United States. Here is the breakdown by state. U.S. overseas territories and Washington DC are also included.

| Location | Designated Opportunity Zones | Low-Income Tracts | Non-LIC Contiguous Tracts |

|---|---|---|---|

| Alabama | 158 | 153 | 5 |

| Alaska | 25 | 25 | 0 |

| American Samoa | 16 | 16 | 0 |

| Arizona | 168 | 160 | 8 |

| Arkansas | 85 | 83 | 2 |

| California | 879 | 871 | 8 |

| Colorado | 126 | 119 | 7 |

| Connecticut | 72 | 71 | 1 |

| Delaware | 25 | 24 | 1 |

| Florida | 427 | 427 | 0 |

| Georgia | 260 | 260 | 0 |

| Guam | 25 | 23 | 2 |

| Hawaii | 25 | 23 | 2 |

| Idaho | 28 | 26 | 2 |

| Illinois | 327 | 327 | 0 |

| Indiana | 156 | 153 | 3 |

| Iowa | 62 | 61 | 1 |

| Kansas | 74 | 70 | 4 |

| Kentucky | 144 | 139 | 5 |

| Louisiana | 150 | 145 | 5 |

| Maine | 32 | 30 | 2 |

| Maryland | 149 | 145 | 4 |

| Massachusetts | 138 | 137 | 1 |

| Michigan | 288 | 283 | 5 |

| Minnesota | 128 | 127 | 1 |

| Mississippi | 100 | 95 | 5 |

| Missouri | 161 | 153 | 8 |

| Montana | 25 | 25 | 0 |

| Nebraska | 44 | 43 | 1 |

| Nevada | 61 | 60 | 1 |

| New Hampshire | 27 | 27 | 0 |

| New Jersey | 169 | 169 | 0 |

| New Mexico | 63 | 59 | 4 |

| New York | 514 | 497 | 17 |

| North Carolina | 252 | 241 | 11 |

| North Dakota | 25 | 25 | 0 |

| Northern Mariana Islands | 20 | 20 | 0 |

| Ohio | 320 | 317 | 3 |

| Oklahoma | 117 | 114 | 3 |

| Oregon | 86 | 81 | 5 |

| Pennsylvania | 300 | 289 | 11 |

| Puerto Rico | 863 | 837 | 26 |

| Rhode Island | 25 | 25 | 0 |

| South Carolina | 135 | 128 | 7 |

| South Dakota | 25 | 23 | 2 |

| Tennessee | 176 | 170 | 6 |

| Texas | 628 | 628 | 0 |

| Utah | 46 | 46 | 0 |

| Vermont | 25 | 23 | 2 |

| Virgin Islands | 14 | 13 | 1 |

| Virginia | 212 | 207 | 5 |

| Washington | 139 | 132 | 7 |

| Washington DC | 25 | 25 | 0 |

| West Virginia | 55 | 52 | 3 |

| Wisconsin | 120 | 120 | 0 |

| Wyoming | 25 | 24 | 1 |

Opportunity Zones Analysis

Number of Opportunity Zones

States and U.S. overseas possessions were able to designate up to 25 percent of eligible census tracts as opportunity zones. Therefore, the number of opportunity zones in each state is highly correlated with the total population of the state. This explains why California, Texas, New York, Florida, and Illinois are among the states with the most opportunity zones, together accounting for nearly one-third of the total.

Puerto Rico is the outlier; their count of 863 opportunity zones is second only to California’s 879. Because of the extensive hurricane damage from 2017, Puerto Rico was granted special status that allowed them to nominate all of their low-income census tracts as opportunity zones. As such, nearly every tract on the island is an opportunity zone.

States and overseas possessions with fewer than 100 eligible census tracts were able to nominate up to 25 opportunity zones. Alaska, Delaware, Guam, Hawaii, Montana, North Dakota, Rhode Island, South Dakota, Vermont, Washington DC, and Wyoming all took advantage of this rule, explaining why each of these locations has exactly 25 opportunity zones. Northern Mariana Islands, American Samoa, and Virgin Islands have fewer than 25 eligible tracts.

Median Household Income

Because only low-income census tracts and certain tracts contiguous with low-income tracts were eligible for opportunity zone nomination, the median household income of all of a state’s opportunity zones is always lower than the statewide average. Certain states have higher levels of income disparity between opportunity zones and their statewide average than others.

In places like Connecticut, Washington DC, and Illinois, the median household income in opportunity zones is 50 percent or less than the statewide average. Conversely, in places like New Mexico, Mississippi, and West Virginia, there is a much lower level of income disparity; median household income in the opportunity zones of these states is greater than 75 percent of the statewide average.

Rural vs. Urban

Some states are more rural than others. The slope of the lines in the chart below illustrate how some states focused on nominating opportunity zones from rural or urban areas of the state. While most states nominated a slightly higher percentage of rural opportunity zones vs. their statewide averages, there are some outliers.

States like Idaho, New Hampshire, Colorado, and Georgia focused on nominating rural areas as opportunity zones (large positive slope on the chart below). Other states like North Dakota, Indiana, Ohio, and Connecticut focused on nominating urban areas as opportunity zones (negative slope on the chart below).

Opportunity Zone are just one of our tax planning tools

Here’s how our in depth tax planning process works

Initial Consultation

We start with a one-on-one consultation to understand your financial goals and tax situation. This helps me get a clear picture of where you stand and sets the stage for building a tailored plan that aligns with your needs.

In-Depth Financial Review

I then conduct a thorough review of your finances, analyzing income, expenses, investments, and existing tax strategies. This step reveals opportunities for savings and improvement, forming the foundation for a successful tax plan.

Tailored Tax Strategy

Next, I design a personalized tax strategy that maximizes deductions, minimizes tax liabilities, and ensures compliance with the latest tax laws. My goal is to help you save as much as possible while reducing stress around tax planning.

Full Implementation

Once the strategy is crafted, I will take care of the entire implementation process. You can trust me to handle the complexities, allowing you to focus on what matters most while I execute your tax plan seamlessly.

Quarterly Reviews

I provide quarterly reviews to track progress, make adjustments, and ensure that your strategy remains effective. This proactive approach keeps you ahead of any changes and ensures that your financial plan stays on track.

Ongoing Year-Round Support

My support doesn’t stop there! I offer year-round guidance, alerting you to any tax law changes and refining your strategy as needed. With my ongoing support, you’ll always be informed and ready for any tax challenges ahead.

AND STOP OVERPAYING

WE REVIEW FOR APPROXIMATELY 1,500 TAX PLANNING OPPORTUNITIES

Below are Just a Few of the Broader Tax Recovery Opportunities That We Review

Cost Segregation

Our Cost Segregation Specialists would identify and reclassify assets. Our results are unmatched; we typically reclassify up to 40% of our client’s assets, providing significant tax savings.

Entity Structuring Review

Our Cost Segregation Specialists would identify and reclassify assets. Our results are unmatched; we typically reclassify up to 40% of our client’s assets, providing significant tax savings.

Overlooked or Underutilized Deductions

Our income tax professionals review past returns, looking for missed opportunities. We have a vast database of the typical deductions broken down by industry to determine if the client utilizing ALL available deductions.

Review Accounting Methods

Federal Tax Accounting methods determine the timing of revenue, expenses, and treatment of inventory and fixed assets for tax purposes. Our income tax professionals conduct reviews of current accounting methods that can aid in planning to meet a taxpayer’s needs, whether to accelerate expenses to reduce taxable income and potentially create a net operating loss (NOL) or allow deferral of expenses in some cases where a taxpayer may wish to increase taxable income for credit utilization.

Fixed Asset vs. Repairs Review

Proper management and classification of fixed assets are critical to an organization’s tax management and compliance objectives. Improper capitalization of fixed assets can substantially negatively impact an organization’s balance sheet, resulting in missed tax savings and added compliance risks.

Our Fixed Asset Review Service provides a comprehensive analysis of fixed assets to determine current asset classifications, ascertain depreciation reported in prior tax returns, and identify potential asset reclassification to ensure every appropriate tax deduction available is claimed.

Tax Credits and Incentives Review

Our tax credit specialists will look for credits and incentives such as the Federal and State Research and Development Tax Credit (R&D), Work Opportunity Tax Credit (WOTC), Section 45L, Section 179D, Energy Investment Tax Credit, Disaster Zone Employment Retention Tax Credit, Federal and State Employment Zones Tax Credit, Differential Wages Tax Credit, FICA Tip Tax Credit, Small Employer Retirement Plans Startup Costs Tax Credit, and Small Employer Health Insurance Premiums Tax Credit. As opposed to deductions, tax credits are actual dollar-for-dollar federal and State credits available to businesses of any size. Many companies are unaware of the broad scope of activities that qualify for these credits. Evolving statutes, IRS regulations, and court cases continue to credit credit and incentive programs for an ever-widening range of qualified businesses.

What Our Clients Say ?

Michael Brown

“We have been using their payroll services for years. They are reliable and efficient.”

Jane Locus

“Their tax preparation services saved us a lot of money. Highly professional and awesome people.”

Martin Frenandez

“The bookkeeping services provided by this company have been exceptional. Highly recommend!”